Mortgage arrears hit 7 year high!

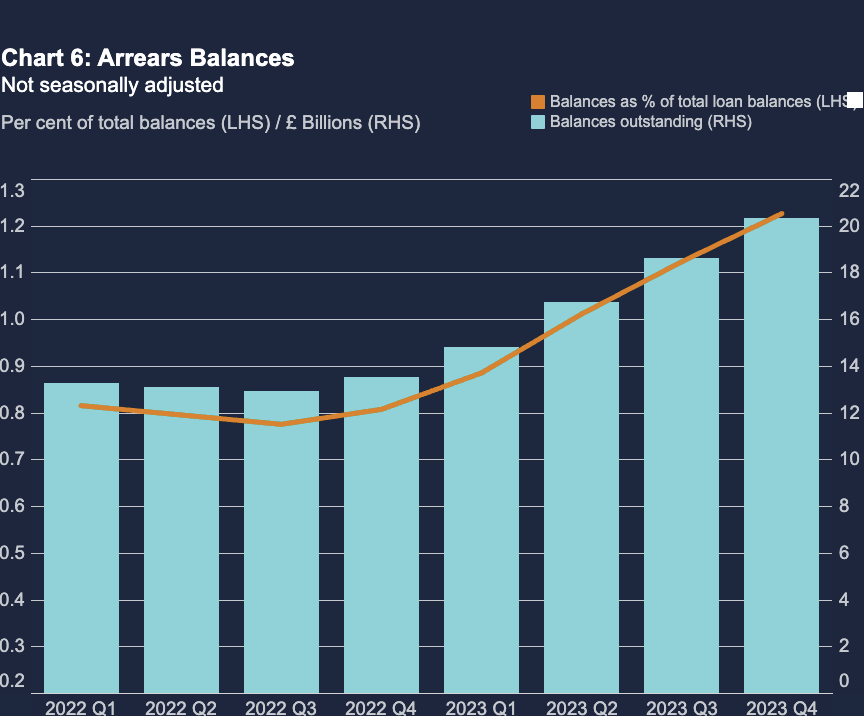

The Bank of England has released quarterly data showing that mortgage arrears increased by 9.2% in the final quarter of 2023. To put that into perspective, it's a 50% increase from the last quarter of 2022.

The numbers

High-interest rates are a major factor. Many families have cut spending, including suspending their mortgage payments. Not all are in arrears due to their inability to afford the mortgage; some have taken advantage of lender schemes to take a payment holiday.

The total value of mortgages with some arrears is approximately £20.3bn or about 1.23% of all mortgage balances. To be considered as having reportable mortgage arrears, a borrower or borrowers must have at least 1.5% of the mortgage balance outstanding as arrears.

In reality, the figure for 1.23% is still quite low. It's more about the pace at which arrears are growing, which is concerning.

There is still likely more pain ahead for borrowers. Around 1.5m are still on low rates due to having fixed rates for a long period, but those low rates end this year, and all will be refinancing or looking to their current lender for a new rate and going from a <2% rate to potentially >5% will hurt, as many already know.

A borrower with a £250,000 mortgage rate of 2% will pay £1,060 monthly. If that rate is increased to 5%, the new payment will be £1,461 per month—an increase of £401.

Stressing mortgages hasn't worked

Since 2014, all lenders have had to start stressing mortgages. The concern was that rates had been so low for so long that borrowers may not be able to handle the shock of spiralling interest rates. So when anyone applied for a mortgage, the lender would test whether it could still be afforded if the rate increased by 3%.

Many in arrears today have seen wages grow, but the reality is that over the years, nobody held some spending back for higher mortgage costs; they spent it on something else or took out other debt that needs to be paid alongside the mortgage.

However, it did restrict borrowing to only those who could demonstrate their ability to withstand higher rates. That may have led to much lower arrears than today, but it isn't easy to tell.

Monitoring arrears is a focus for lenders and regulators alike; it will be a much-discussed topic for some time ahead.

Lee Wisener, CeMAP, CeRER, CeFAP

Having worked in the mortgage industry for over 20 years I have always wanted to build a website dedicated to the subject. Also being a geek when it comes to the internet all I needed was time and I could both build the site from scratch and fill it with content. This is it!

<< Newer Post

Debt Awareness WeekOlder Post >>

What is Fiscal Drag and how does it affect you?